In Part One of this series, we explored key tax and charitable planning strategies to help you make the most of the 2025 year-end. Building on those foundational steps, Part Two shifts the focus to broader wealth considerations—including estate planning, portfolio positioning, and retirement readiness. Together, these components create a more complete, long-term financial picture to help ensure your goals remain protected well into 2026 and beyond.

Estate Planning

Review Estate Plans and Consider Using the Lifetime Gift Tax Exemption

High-net-worth individuals received much-needed clarity as it relates to the federal estate exemption, as the One Big Beautiful Bill (OBBB) permanently set the basic exclusion amount (BEA) to a base of $10 million per person plus inflation adjustments. The federal estate exemption is set at $13.99 million per person in 2025 and will increase to $15.00 million per person in 2026.[5]

While the fear of the favorable estate exemption sunsetting at the end of 2025 to a reduced base (possibly to $7 million per person) is no longer a concern, high-net-worth individuals should still review their current estate plans. It remains important to consider whether utilizing a portion of the lifetime gift tax exemption is appropriate, as a completed gift removes future appreciation from one’s taxable estate.

Make Annual Exclusion Gifts

Individuals are allowed to make “annual exclusion gifts” which do not have gift tax implications. In 2025, the annual exclusion is $19,000 per donee.6 For high-net-worth individuals with a potential or existing taxable estate, utilizing annual exclusion gifts can be an effective way to reduce one’s taxable estate while also providing financial support to loved ones.

Example*: Consider Jim and Mary Donaldson, a very wealthy couple with two married children (four spouses total) and six grandchildren. In 2025, the Joneses, as a couple, could gift $38,000 to each of the ten individuals for a combined total of $380,000, without such gifts counting against their lifetime gift tax exemption. By regularly making annual exclusion gifts, the Joneses are able to gradually reduce the size of their taxable estate, while also providing meaningful financial support to their family.

*For illustrative purposes only.

For those saving for future college expenses, special rules allow a donor to use up to five years of annual exclusion gifts for contributions to 529 college savings plans (a limit of up to $95,000 for a single taxpayer or up to $190,000 for joint taxpayers, as of 2025).7 It is worth noting that medical payments made directly to a medical provider do not count as taxable gifts. In addition, tuition payments made directly to an educational institution do not constitute taxable gifts. Tuition is narrowly defined as the cost for enrollment; it does not include books, supplies or room and board.

Plan for the Unexpected

A good estate plan should prepare for the unexpected. While it may be difficult to think about what would happen in the event of one’s incapacitation, it is critical to have documents in place which spell out who is entrusted to make important financial and medical decisions. Important “must-have” estate planning documents include a durable power of attorney for finances, a health care proxy (essentially, a health care power of attorney) and an advanced care directive. Individuals with children who are minors should have a will which names a legal guardian.

Review Beneficiary Designations

Individuals should review financial accounts and insurance policies to ensure the recorded beneficiary designations align with their intentions. “Life events” such as marriage, divorce, birth/adoption, etc. should serve as an important point to review and update such designations.

Investment & Retirement Planning

Revisit Portfolio Allocations and Longer-Term Investment Objectives

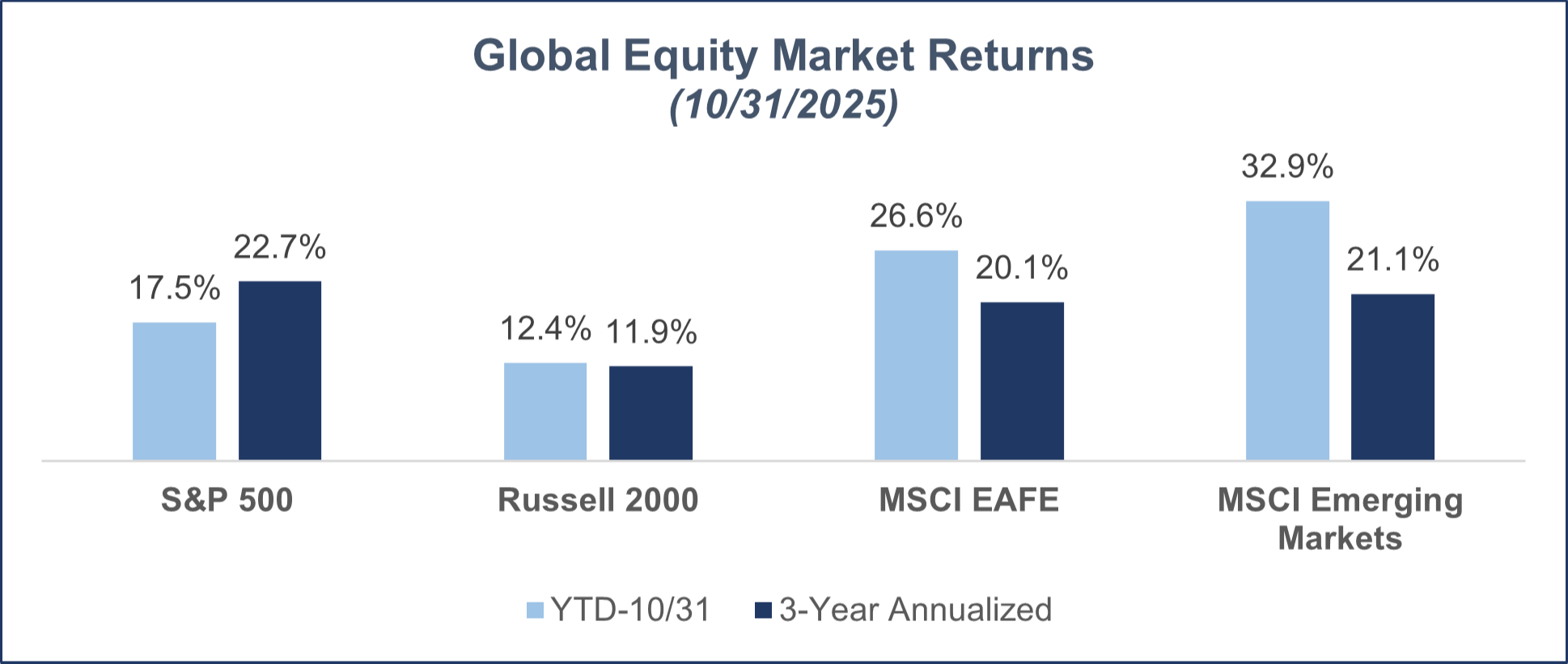

Global equities (and U.S. Large Cap equities, in particular) have generated significant gains over the last several years.

Source: Morningstar, as of October 31, 2025.

Following an extended rally among risk assets, investors may fall into a sense of complacency over portfolio risk or, worse yet, may “chase returns” at an inopportune time. Ideally, an investor should have an investment plan anchored to risk tolerance, time horizon and longer-term goals to avoid making emotional, reactive investment decisions based on the current market environment.

Investment goals can change over time and a portfolio’s allocation should be flexible to adjust accordingly. The changing market landscape can also make certain investments which were less appealing previously to be more actionable at other times. Regularly reviewing a portfolio’s allocation among cash, fixed income, global equities, real assets, and, if applicable, alternative investments against longer-term goals is a critical exercise for investors.

Assess Portfolio Tax-Efficiency

Investors should think of their portfolio as an allocation among several different buckets: after-tax (taxable investment accounts), pre-tax (traditional retirement accounts) and no-tax (Roth retirement accounts). Rather than holding similar investments across all investment accounts, an investor should instead consider the “asset location” of investments designed to minimize tax drag to the greatest extent possible.

First, high-growth investments (such as global equities) should be allocated to Roth retirement accounts, given the favorable tax treatment afforded to Roth accounts. Actively managed equity mutual funds may be given additional consideration as capital gain dividends will not have tax consequences while produced inside the Roth account. Next, traditional retirement accounts (such as an IRA, 401k/403b, etc.) should hold less tax-efficient asset classes, such as taxable bond funds and REITs which produce non-qualified dividends, which are taxed at ordinary income rates. Finally, taxable accounts should be structured to “round out” the portfolio to get to a desired target allocation. In general, taxable accounts should hold more tax-efficient investments, such as equities which generally produce favorably taxed income (qualified dividends), and should evaluate whether to hold taxable or tax-exempt bonds, depending on an individual’s tax bracket.

Maximize Retirement Contributions

According to Vanguard’s “How America Saves 2025” report, only 14% of Vanguard plan participants contributed the maximum amount to their 401(k) plan in 2024.8 Individuals who are still actively employed should review their year-to-date retirement contributions and evaluate whether to make additional contributions prior to year-end.

- The basic employee 401(k)/403(b)/457 contribution limit is $23,500 for 2025.9

- The catch-up 401(k)/403(b)/457 contribution limit for employees age 50 or older is $7,500 for 2025).10

- The IRA contribution limit is $7,000 for 2025.[8]

Under SECURE Act 2.0, effective for January 1, 2025, some individuals may have an increased retirement savings opportunity. In 2025, individuals 50 or older will have a 401(k)/403(b)/457 catch-up limit of $7,500; however, SECURE Act 2.0 includes a new provision for employees aged 60-63 to utilize an enhanced catch-up contribution limit of $11,250 (instead of $7,500). It is important to note that each Plan Sponsor will decide whether to implement this enhanced feature in their retirement plan.

Finally, individuals who are still working should assess whether to increase their contribution percentage for their 401(k)/403(b) for the next year and should consider whether to save to their employer retirement plan on a pre-tax basis (traditional contributions), on an after-tax basis (Roth contributions), or a combination of both pre-tax and after-tax contributions.

For personalized advice on how these strategies might benefit you, please reach out to a member of our private client team.

- [5] Source: Forbes – “Estate Planning and The Final OBBBA: Key Changes High-Net-Worth Individuals Must Know” (July 3, 2025)

- [6] Source: IRS – “IRS releases tax inflation adjustments for tax year 2025” (October 2024)

- [7] Source: Fidelity – “529 contribution limits for 2024 and 2025” (February 28, 2025)

- [8] Source: Vanguard – “How America Saves 2025”

- [9] Source: Forbes – “IRS Announces Retirement Contribution Limits Will Increase Will Increase In 2025” (November 2024)

- [10] Source: IRS – “401(k) limit increases to $23,500 for 2025, IRA limit remains $7,000” (November 2024)